Did the government waste tens of millions of pounds extending the lives of construction firms that were beyond saving?

Three years ago, as unprecedented social and economic restrictions were introduced to battle Covid, then chancellor Rishi Sunak set the tone for a huge package of emergency government support for business. “The coronavirus pandemic is a public health emergency,” he declared. “But it is also an economic emergency. We have never in peacetime faced an economic fight like this one. I know that people are deeply worried. I know that people’s anxiety about the disease itself is matched only by their anxiety about their livelihoods.”

Available from April 2020, the Covid business support schemes were meant to save companies from going under when whole sections of the economy were shuttered. By the end of 2022, however, construction companies were going bust at their fastest rate in over a decade. So were the schemes a success? Did they offer enough support to contractors? Or did they waste public money on companies that were already doomed?

Analysis by Construction News of more than 1,000 Companies House filings reveals that at least a quarter of construction firms going into administration or receivership since April 2020 had obtained Covid loans.

Table of Contents

Breathing space

Unlike furlough claimants, the names of those that used the loan schemes have never been released by the government. In January, the government won a legal case against transparency campaigners – who were concerned with naming fraudsters – ensuring that the borrowers could remain secret. Aside from fraud, transparency about the system would also help to assess how successful the schemes were, by enabling examination of the financial health of the companies that received loans.

“It was a commercial loan, it wasn’t a hand-out. We took it thinking life was going to get back to normal a lot quicker than it did… but Covid carried on”

Jonathan Wildgoose, Wildgoose Construction

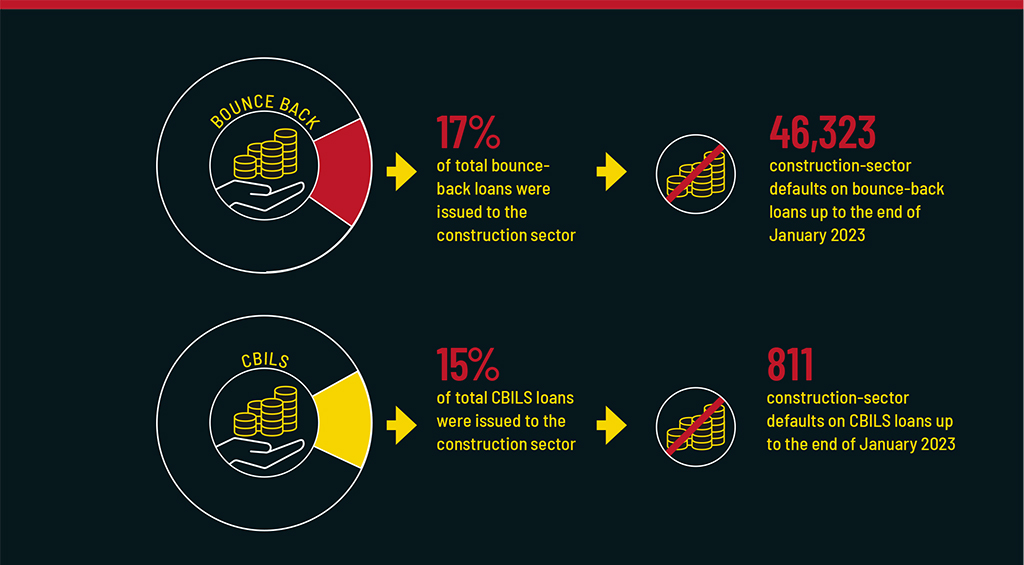

The three main schemes introduced in the period were bounce-back loans of up to £50,000 for small firms; the coronavirus business interruption loan scheme (CBILS), offering companies with turnover of up to £45m loans of up to £5m; and the coronavirus large business interruption loan scheme (CLBILS), enabling borrowing of up to £200m for firms generating higher revenues.

Other types of finance, such as overdraft facilities, were also made available. Lending institutions received guarantees of between 80-100 per cent from the taxpayer.

Official data shows that construction companies received more than £11.69bn from the schemes before they closed on 31 March 2021. The support provided “much-needed breathing space and reduc[ed] cashflow concerns for many,” Catherine Lewis La Torre, then chief executive of the British Business Bank, which operated the bounce-back scheme and CBILS, said in July 2021.

Yet critics say that the breathing space was artificial, merely keeping badly performing companies alive for only a few months longer than they otherwise would have survived – and at a huge cost to the taxpayer.

First to go

CN examined official filings from 592 companies captured in monthly administration round-ups based on data provided by Creditsafe. Of those, 137 used the schemes, with a further 13 having the same owners as another firm in the first group (see methodology box, below).

In the early weeks of the pandemic contractors and trade bodies complained that lenders were pushing construction companies towards other types of finance instead of the loans. This prompted Whitehall to intervene and make banks lend more easily. But by October 2020, the first two contractors to borrow money through the schemes had filed for administration.

York-based Evora Construction and JA Ball of Leicestershire had each obtained bounce-back loans but the cash injections were unable to save them from the impact of the new restrictions.

In the same month, £12m-turnover leisure centre specialist Createability also went under. With its clients hit hard by lockdown, the Southampton-based firm sought to get £500,000 through a CBILS loan shortly after the scheme opened and before borrowing was made easier. It was turned down by three different institutions.

Ian Cotgrave had built the business over 26 years, from a sole-trading outfit to one that employed 36 people. It had never borrowed money before. In 2019 it was hit by a bad debt from a non-paying client that put itself into administration when Createability threatened legal action. “He took us for about £1m,” Cotgrave recalls. “But we still had money in the bank and we were still trading. Just as we were starting to recover and had about £11m-worth of business on the books ready to come in, Covid struck and the leisure industry shut its doors.”

The bad debt meant Createability’s latest set of accounts were loss-making – for the first time in its history – so it was refused the loan from all three lenders. “The ironic thing is we were a highly profitable company apart from one debt… and yet I know of companies that were borderline [and] should’ve shut the doors quite a few years ago, but because they were still making a marginal profit [they] qualified for the loan,” Cotgrave says.

A management buyout had been examined before lockdown, which would have helped Cotgrave move towards retirement. The plan had to be shelved amid the turmoil. “I used to reinvest almost everything back into the company, so lost the company and all the money that was in it,” he says. “We did have a good reputation and the day we shut the door was very sad.” Cotgrave, who now works as an independent consultant, praises the furlough scheme as “brilliant” but feels the government should have offered more support for construction businesses.

The borrowers

However, more than 275,000 loans were issued to construction companies in total, with the largest single loan found in CN’s analysis going to £64m-turnover WRW Construction (see table, below). But Llanelli-based WRW was the largest industry failure in 16 months when it filed for administration in July 2021, after losing an adjudication on a contractual dispute that exacerbated existing cashflow problems. Administrators Grant Thornton said it had obtained a £5.1m CBILS loan from ThinCats in June 2020. Despite being a secured creditor, the lender is not expected to recoup all its money through the administration and the taxpayer will likely pick up some of the cost.

In April 2020, troubled NMCN announced it would look at using a CLBILS loan. The £400m-turnover contractor went under in October 2021, but its administrators subsequently said it had not claimed from the scheme.

Wildgoose Construction, which had a £52m turnover, obtained a £1.5m CBILS loan from NatWest in October 2020. Nevertheless, it filed for administration in November 2021. “It was a commercial loan, it wasn’t a hand-out,” explains Jonathan Wildgoose, former chairman of the Derbyshire firm. Obtaining the loan required cross-guarantees and a detailed business plan. “We took it thinking life was going to get back to normal a lot quicker than it did. We got the loan on the back of our business plans which were extremely well put together but [what we expected] just didn’t happen because Covid carried on.”

The 100-year-old family firm had been operating on small margins “hoping to make a 1 per cent profit” prior to the pandemic, he says. He adds that the industry was not in a good place pre-Covid – battered by Brexit, falling government spending, a rush towards using frameworks and a slowdown in the planning system. “The CBILS loan was a good idea but it didn’t really cover the fact that things got worse and worse,” he says, citing material shortages, increasing costs and the impact of fixed-price contracts, with some clients not making allowances for these.

Wildgoose also feels that the furlough scheme went on too long for construction, compounding labour shortages. But a race to the bottom on bidding was the biggest issue, with the profit available often not making sense compared with the penalties associated with possible delays. “The construction industry is basically its own worst enemy,” he says. “It was a huge disappointment to me that we ended up where we were. It was just an impossible situation.” NatWest was paid back in full after the sale of the company’s headquarters. Its development sister-company Wildgoose Homes continues to trade.

Time will tell

In many cases, the loans did not start being repaid until months after they were taken out and most were interest-free for the first year. More recent administrators’ reports show that these repayments became a burden on companies contacting liquidators. For many, pressures of energy costs after the onset of the Russia-Ukraine war were piled on top of the costs of paying back the loans.

In July 2022, all but five of the 23 firms entering administration had claimed through the loan schemes themselves or were part of a group of companies where another entity did. But a final judgement on the scheme’s success will be impossible for several more years, with firms having up to 10 years to pay back the money.

Most of the administrations examined are also incomplete, and many reports are unclear about lenders’ prospects. However, many of them were listed as unsecured creditors, meaning the taxpayer is expected to pick up much of the cost.

Some commentators feel that the loan schemes were too generous and kept many “zombie companies” alive. Chris Davies, managing director of DRS Bond Management, says: “People were given loans from banks that would never normally give them loans at all because of the government guarantee that sat behind the schemes. Today, if you’re looking for funding as a construction company those facilities are definitely not available, and they won’t be available again.”

Cotgrave says: “In hindsight would getting a loan have made any difference? Possibly not, the way Covid just dragged on and on, we may have got to a situation where we may have had to have gone into administration at a later date.” But he says it would have bought Createability some time to try to diversify beyond the leisure-centre sector.

For Davies, many companies going into April 2020 in a weak position were thrown a lifeline, but “the clock was ticking down and down” and a lot of public money will end up being lost. “With the benefit of hindsight, a lot of Covid policy around a variety of things doesn’t appear to have done well.”

Others are less critical. Christina Fitzgerald, president of insolvency trade body R3 and Edwin Coe partner, says: “Covid was something that nobody saw coming and required the government to find a means of supporting businesses right across the economy almost overnight after lockdown was introduced. They had a difficult line to walk between making the support accessible to businesses who needed it and putting checks and balances in place – which might have been the difference between a company surviving or not.”

Top 20 covid support loan borrowers that went into administration |

||||||

|

Company |

Location |

Type of business |

Administration or liquidation date |

Type of loan |

Latest turnover (£m) |

Amount borrowed (£m) |

|

WRW Construction Ltd |

Llanelli |

Main contractor |

Jul 2021 |

CLBILS |

64.00 |

5.10 |

|

Fireclad |

Essex |

Drylining specialist |

Jun 2022 |

CBILS |

13.20 |

3.00 |

|

Mid Contracting and Consulting Ltd |

London |

Offsite specialist |

Aug 2022 |

2x CBILS |

55.00 |

3.00 |

|

Vital Infrastructure Asset Management (VIAM) Ltd (formerly registered as Knowsley Contractors, traded as King Construction) |

Liverpool |

Highways and utilities |

Jun 2021 |

CBILS |

36.00 |

2.90 |

|

Dickinsons (Plumbing & Heating |

Leeds |

Plumbing, heating and renewable energy services |

May 2022 |

CBILS |

7.90 |

2.80 |

|

Brymor Group Ltd (parent company of |

Hampshire |

Main contractor |

Jul 2022 |

CBILs |

82.00 |

2.00 |

|

Hippocampus Group Ltd (formerly called |

Antrim |

Marine civil engineering |

Feb 2022 |

CBILS |

13.70 |

1.75 |

|

Wildgoose Construction Ltd |

Hampshire |

Main contractor |

Nov 2021 |

CBILs |

52.50 |

1.50 |

|

O'Keefe Construction |

London |

Ground and civil engineering |

Jul 2022 |

CBILs |

61.00 |

1.50 |

|

Crossfield Construction Ltd |

Liverpool |

Main contractor |

Apr 2022 |

CBILS |

Not published |

1.00 |

|

Architectural Fabrications Ltd |

Sheffield |

Metalwork producer |

Nov 2021 |

CBILS |

4.90 |

0.92 |

|

Goodwin’s Construction Services Group Ltd |

Manchester |

Main contractor |

Nov 2020 |

CBILS |

10.20 |

0.70 |

|

Kapex Construction Ltd |

Newcastle |

Residential contractor |

Aug 2021 |

CBILS |

15.00 |

0.69 |

|

TA Boxall & Company Ltd |

Surrey |

M&E specialist |

Nov 2022 |

CBILS |

Not published |

0.63 |

|

Horizon Controls Ltd |

Sheffield |

Building management solutions |

Nov 2022 |

2x CBILS |

Not published |

0.60 |

|

Mitch Cassin Groundworks & Construction Ltd |

Birmingham |

Groundworks |

Aug 2021 |

CBILS |

Not published |

0.50 |

|

OEP Building Services Ltd |

Lancashire |

Bathroom pod manufacturer, supplier and installer |

Nov 2021 |

CBILS |

8.60 |

0.50 |

|

Bexheat Ltd |

London |

MEP contractor for apartment new-builds |

May 2022 |

CBILS |

Not published |

0.50 |

|

Harris CM Ltd |

West Yorkshire |

Main contractor |

Aug 2022 |

CBILS |

27.00 |

0.50 |

|

Intex Systems Ltd |

Manchester |

Maintenance, drylining and cladding |

November 2022 |

CBILs |

Not published |

0.50 |

The methodology

Construction News examined Companies House documents relating to all of the construction-related firms that appeared in our monthly

round-up of administrations/receiverships between April 2020 and December 2022.

The data, provided by Creditsafe, includes developers, manufacturers and contractors.

Other high-profile cases of contractors that moved straight to liquidation (and don’t appear

in the round-ups) were also examined.

More than one filing was looked at in the majority of cases.

The amount of information provided in each case differed, with the amount borrowed unclear in several cases and others not stating clearly the type of loan issued. Seventeen firms stated they had borrowed but did not put a figure on the level.

Due to the lack of clarity in many reports, the number of companies making use of the schemes and going under in these months is likely to be higher than the 137 stated.